5:50 When buying a house how soon should I talk to a lender?

7:38 What factors affect my credit score?

10:20 Why do people use their credit card like it’s not their money?

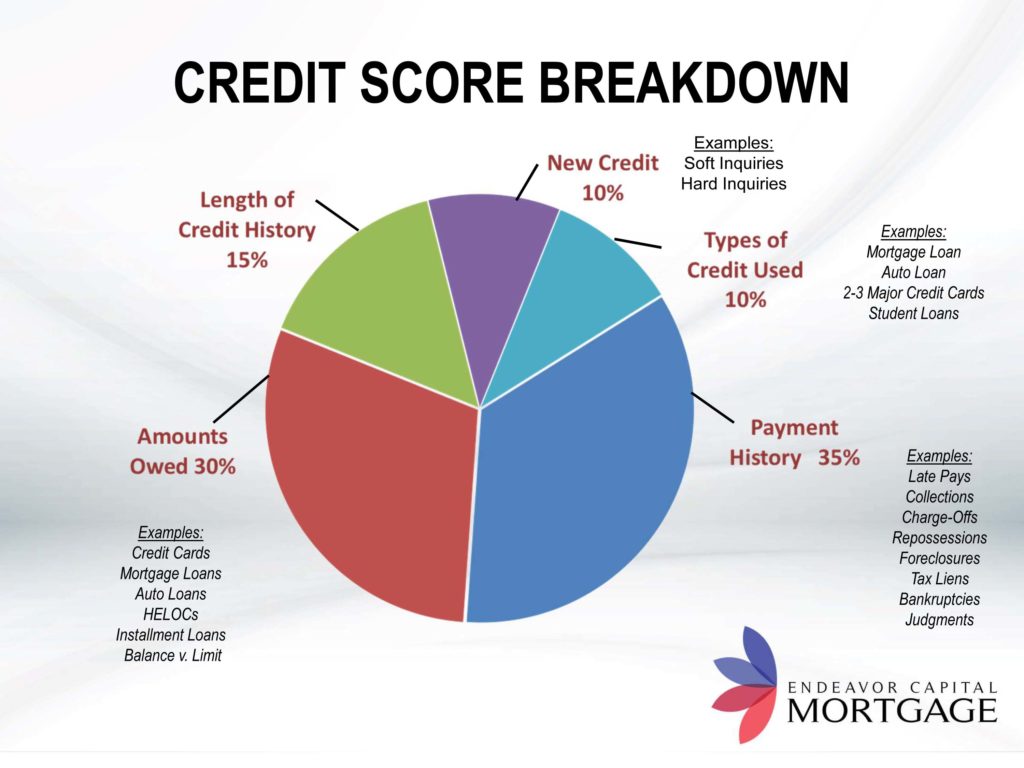

11:19 35% of your credit score is your payment history

12:54 Will paying an old collection off help or hurt my credit score?

13:50 How long does it take for an old collection fall off of my credit score?

14:48 What is a charge off?

15:28 Does every creditor report to the credit agencies?

17:05 30% of your credit score is amounts owed a.k.a. your credit utilization rate

18:18 What is a rapid rescore?

24:40 Is it a good idea to pay down an auto loan faster?

26:25 15% of your credit score is length of credit history

27:55 What is the difference between a regular credit card and a secured credit card? Should a parent get their teenager a secured credit card?

30:00 10% of your credit score is new credit

30:40 What is a hard pull/ inquiry and does it drop your credit score? What happens if my credit is checked multiple times in a short amount of time?

31:50 What is a soft pull and does it drop your credit score?

34:45 Should I cancel a credit card that I’m not using?

37:25 10% of your credit score is the type of credit used

39:51 What is the highest credit score George DeMare has ever seen in 25 years?

41:16 What is OptOutPreScreen.com and how does it help cut down on the junk mail?

41:45 Contact George DeMare by calling 314-378-0331 or emailing GDemare@ecapmortgage.com

TRANSCRIPTION

Live on the rooftop of the Hermann London real estate group in beautiful downtown Maplewood it’s the St. Louis Realtor podcast with your host Adam Kruse welcome welcome everybody to the St. Louis Realtor podcast live from the rooftop of the Hermann London real estate group in beautiful downtown Maplewood Missouri I’m your host Adam Kruse here with my co-host Shannon Shannon St. Pierre also a Realtor here with Herman London and we’re super pumped to have in today our expert lender mortgage guy credit guy good friend George Demare from Endeavor Capital Mortgage thank you that’s a nice introduction yeah well thank you for being here you know I know you had lots of places to do you probably close in tons and tons of loans today but we really you know we did for our listeners we did podcast number 41 was all about credit repair and so we brought George in here today because Shannon and I really wanted to talk more about credit it’s such an important topic it seems to really drive people’s lives and so today we’re gonna talk about the myths of the credit score and George is gonna sort of break down what makes up a credit score and and we have lots of interesting questions for him too a lot of misconceptions out there on what makes up your credit score so those are some of the things you want to clear up for our listeners today but before we jump into that can you tell me kind of like why credit matters you know you know what I mean yeah absolutely so credit in our world today is more important than ever most people think it just affects the interest rate you’re gonna get on your mortgage maybe the interest rate you’re gonna get on a car loan something like that but above and beyond that it’s now crept into the insurance world so you think about what we all do here is selling houses and doing mortgages on houses everybody needs homeowners insurance your homeowners insurance companies now are pulling a credit report on you and the premium you pay is based off of whatever your credit score is that’s one of the factors that looking at credit cards you know are you gonna get the primo interest rate on your credit card well if you don’t have a 740 score above you’re probably not so if you got a 600 credit score you’re gonna get a credit card that’s gonna have a higher interest rate on it if you’re carrying a balance okay and you know they always stay like the rich get richer and stuff like that and I guess this sort of plays into that right because in theory the rich quote-unquote don’t have big debts out there they don’t have they they have a good credit score essentially and so they’re able to get access to more money for cheaper or whatever right yeah and I think the goal is is what we’ve done with Endeavor Capital with Herman London with you guys is we’re trying to educate our clients so if they don’t have a great credit score right now what can we do to help you improve your credit score and I think that’s a lot of what we’re gonna talk about today so that people who maybe aren’t making a ton of money and have a great credit score right now can we get them there and then they can call their mortgage company Endeavor Capital Mortgage and potentially refinance get a better rate can they look at their car loan that they currently have refinance that get a better rate call their homeowners insurance company that’s one of the biggest things that people forget about because most times we escrow for your homeowners insurance and your real estate taxes so a lot of people forget about that when each year you should be doing a check up on your homeowners insurance as well as your mortgage just like you go to the doctor and get your yearly checkup why not shop your homeowners insurance and if we’ve gotten your credit scores to increase chances are you’re gonna get a lower premium which means a lower monthly mortgage payment seems like there’s so much to keep up with you know or we’re trying to get we’re trying to encourage people if it’s the right fit for them to buy homes and get mortgages and stuff and like you said these are things you’re supposed to be checking up with every year not only maintaining the home but we’re supposed to be checking up on our rates and all these things we’re just saying you should also check up on your credit score and kind of maintain make sure that you’re maintaining a high credit score you know doing the right things to raise your credit score yes agree 100 percent once a year you should actually be pulling your credit and what I recommend is going to a site called annual credit report.com that is a free site you can pull a credit bureau on all three of the credit repositories will show up on there and it will give you an idea on where you are it also lets you know are there any mistakes on your credit report that’s one of the things Adam that we’re gonna talk a little bit about today is we also see a lot of mistakes people have trade lines that are showing up that maybe it’s they’ve got the same name as their dad and it’s showing up on their credit report or a collection that they didn’t even know about because they haven’t had their credit pulled in several years so we want to look at it at least once a year and make sure that everything’s accurate and everything is correct if a credit report doesn’t tell you your score which is a lot of people go on and get their credit report looking for the score but that score is is separate of the credit reports and I feel like it doesn’t even matter anyway and you can see your credit score would most I think credit cards now as well that’s real ever but it still doesn’t matter that credit score is not the same as the credit score that you have with mortgages and stuff like that so we’ll kind of touch base on that but they think that kind of back up just for a moment when we talk about the credit and in terms of our clients and wanting to buy a house one of the things I highly highly encourage my clients and I think you do too is talk to a lender as soon as possible to kind of go through the credit report because in our heads we think that it’s to our best advantage to maybe pay off a credit card and in essence that may not be the best approach in in regards to your credit score and raising it and so I always have them talked to a lender to potentially get a strategy to help raise the credit score if needed but because it’s not what’s you know intuition yeah that’s great advice people seems like sometimes they get insulted you know for like call George talk to him about your pet a pre-approval have them run your credit and all that stuff and they think I have a good job I make good money why are you insulting me by saying that you don’t trust me or something like that you know but it’s not about that right it’s about like well and that’s why I did it scores are there’s so many myths number one revolving around them but number two it’s this extremely difficult puzzle that no one can truly tap down it’s just we have an idea but there’s no real solution to the puzzle I’m gonna ask you just a couple times George but can you just give us your phone number three one four three seven eight zero three three one cool okay well do you want to jump in to you you’ve given us this handout that we will post it on our website along with the podcast and it’s got this pie graph pie graph I guess pie chart yeah you have this pie chart on it I want this big piece here and so you’re gonna want to jump in there and kind of start giving us some examples yeah so the first thing that I want to talk about is and you know we’ll use you two guys as examples so Adam let’s say that you make $100,000 a year you’ve been on your job for ten years and you’ve got five hundred thousand dollars in the bank and Shannon you’ve been on your job for a year you’re making $40,000 a year and you’ve got two months of bills in your bank account would you say you know just to start us off here that you would probably have a better credit score than Shannon based on what I just said yes okay so I’d say now so we both know now who took my class Shannon was in my credit scoring class Adam skipped out because he would know the answer to this which is none of those factors have anything to do with your credit score okay how about that but you wouldn’t okay so honor you wouldn’t say that it’s more likely that someone who has a bunch of money or whatever has better credit well whether they have better credit or not we don’t know but does that factor into what your credit score’s those specific things your actual salary or what you’d make your income that’s an action to your credit score or savings how much money do you have in the bank how long have you been on your job know the pleasure on of that applies and a lot of people think that that factors into their credits were being higher when we’re gonna break down and we’re going to talk about the five things only these five things will spit out your credit score on what it’s going right and so the logic would tell you that I’m gonna pay cash for a car or I’m gonna try and pay cash for my groceries all these things cuz I don’t want to get into credit card debt because it’s bad and my parents got into that and we we struggled and all these things are wrapped around credit cards and the feelings and the emotions of money and kind of come from you know our past and our histories and our parents and how they handled it but it’s not what you would it’s not and so a lot ik I mean I see a lot of young people using cash trying to stay away from that debt that issue other than maybe student loans and that’s one of the biggest things we see especially with first-time homebuyers if we’re looking at somebody who’s operating strictly on cash a lot of times they won’t have a credit score when we pull their credit so or it’s very very low yeah I’ve had that many a few times yeah because there’s nothing on there for the algorithm for the credit score to create because they think they’re doing everything right yes it’s interesting because I do almost never use cash I use credit card for basically everything I can if I can even if I have cash in my pocket but I’m super careful about paying the credit card off every month which is very important and I guess some people get into a thing where they get a credit card and then they they just like somehow start spending like it’s not their money or something yeah well yeah it’s easy to do the credit card for your groceries and your gas and oh this little thing up here and that little thing and then by the time you get your credit card bill it’s wrapped up to something right that’s higher than what you had in your head I’ve been watching the rear watching Parks and Rec and I don’t know if you guys but they all they have that treat yourself day and that’s it reminds me of someone like with their credit card for the first time they’re just like treat yourself and when I was in my early twenties in college I got a credit card when a free t-shirt to sign up for the Cardinals I probably did yeah yeah t-shirt they probably never wore but yeah it was and then it was Christmastime and I thought I’d go buy Christmas gifts for my siblings and you know thought I’d do something nice and and for those things no luckily luckily yeah it but yeah it’s easy to rack it up and I can see how it happens yeah so if we want to dive into this yeah you know let’s start off with the biggest percentage which is 35% of your credit score is your payment history I mean it’s as simple as that how do you pay your bills every single month and one thing I want to point out here is if you pay your bills on the 15th of the month for example your mortgage is normally going to be due on the first if you don’t pay by the 15th you are gonna get hit with a 5% late fee but that is not going to report to the credit bureaus negatively against you not until you actually go 30 days late so if you’re more that we’re encouraging you to pay your mortgage late no we do not want to do that because that will really hurt your score but I want to just clarify for people out there that if for whatever reason you forgot or something came up it happens it happens and you make your payment on the 17th of the month you’re gonna get a 5% late charge but that’s not gonna go against you on your on your credit report so 35% of your overall score how do you pay your bills and to take that one step further you can end up being 30 days late on a credit card on a mortgage on an installment loan if you go 60 days late it’s gonna hit your score even harder if you go 90 days late it’s gonna hit it even harder so that’s the the benchmarks on what the credit bureaus are looking at is 30 60 90 and so forth out on that and so some examples of your payment history though that do affect your credit score are not only late pays but collections charge-offs repossessions foreclosures yep and that’s one of the bankruptcies judgments yeah so we’re talking misconceptions here Shannon so one of the biggest misconceptions that I see a lot of people make this mistake you’ve got a collection that’s 5 years old it’s from AT&T you don’t even remember about it whatever the case may be it’s 95 even know about it right and before you get your mortgage you think hey I want to get everything cleaned up on my credit report I’m gonna pay this collection off and in actuality even though that goes against all of our traditional mindset if I’m doing something good again intuition yeah it’s hurting you Roger like admitting guilt yeah you can look at it that way you’re admitting guilt but you’re also bringing that collection back to life as of 2019 when you had that initial collection in 2014 each year that goes by it’s starting to a little bit help you with your credit scores and eventually it will fall off of your your credit report if you pay it off it brings it back to life as the 2019 and your credit score is gonna take a hit for that so when does it fall off generally after seven years okay yeah there’s one you’ll see it fall off so what should you do if you if you need if you have something that was in collections from five years ago or whatever so I think the first thing you should do is is talk with a lender who is experienced in the credit score model and understands credit scores and how they work so when you guys were talking earlier about you you like to send your clients to get them pre-approved with a mortgage company before you even start showing them houses I think at that point that’s when a good loan officer will sit down and review a credit report with their client go through every single thing and then we also have the ability to look and see hey if we do certain things we can get your score increased by a certain amount which entail we’ll get you a better interest rate when we’re all said and done but the goal is is we want to make sure we get them in that house so we want to coach them and make sure that they’re doing all the correct things yeah so don’t touch those collections if they’re same you give another example of a charge off can you guys tell me what is it charge off so basically a charge off is is if you have a delinquent debt with a creditor at a certain point they will write that off as bad debt a delinquent debt like what we were just talking about where you haven’t paid it in four years or whatever yeah they’ll write that off as bad debt so a lot of times what they’ll do is they’ll just charge it off and it’ll show up on your credit report as a charge off and how does it do that like if I owed Blockbuster Video $80 for haha Matilda in 2014 or whatever like and they just go forget it we’re not even gonna go after him for this money how does the credit company or the credit score companies find out about it well because blockbusters are reporting that to the credit agencies not not every creditor reports to the credit agencies there’s three main credit agencies TransUnion Experian and Equifax so most creditors report but there are certain ones that won’t blockbuster I’m not sure I thought you were younger than me I don’t even remember blockbuster but what he is a lot younger than me can I mean this is maybe a little bit off-topic but how do we how today or how do we report so for example we you know we collect a lot of people’s rent for all the properties that we’re managing and we did talk about that right should we be reporting that you can report that if you want that obviously helps clients quite a bit but there’s a process that you would have to go through in order to report that to the three credit agencies and so is it a hard process long process does it cost sounds like there probably be a process for us to establish that we’re legit with them yes yes and and to be honest I’ve never done it before as a creditor so not a hundred percent sure how it works but I do know that we have and we’ve seen people where their property management company is reporting rent to the credit bureaus so that’s something that you guys may want to look into well ideally we like to help our tenants turn into buyers you know who worked with you on that a lot and so if we can help them raise their credit score if that’s what’s keeping them from buying it might be worth it for our company to do yeah it’d be good to do just because they have something positive to outweigh the negative that may exist building them back – yeah I think that would be a great service that you guys could do for your your leasing clients okay so I guess we can segue into PI piece number two the second largest piece of the pie yes 30% a mystery was 35 amounts owed amounts owed is 30% you will often hear this referred to as your credit utilization rate and what that simply means is is when you get a credit card they will give you a high balance on your credit card so let’s say you get a credit card and they give you a high balance of $10,000 the high limit the high limit I’m sorry yes so basically what that means is is you have the ability to go up that high but you need to understand how it’s going to impact your credit score so we had talked about you know paying off your credit cards every month obviously that’s the best thing that you can do but is it because I’ve heard both way so you pay it off yes but then you don’t have revolving well we have revolving debt because the credit card is a revolving debt so we do have a history of seeing because it depends on what day we pull a credit report okay so your balance may be on there because you haven’t paid it yet for the month or the creditor hasn’t reported it to the credit agencies yet so it all depends on what day we pulled that credit report but we can always do a rapid rescore is what we call it and show that your balance is down to zero and that you’ve paid that account off okay so as long as you’re using that credit card that’s what we want to see is is usage data so if you are in a situation where you’re forced to keep a balance we really would like to keep that balance under 30 percent of your high credit limit so back to our example at $10,000 if you can stay under $3,000 if you’re carrying a balance that’s where we want you to be so thirty percent of the credit card limits high credit limit that’s correct but that’s carrying over balance because say you have like a ten thousand dollar credit limit and you put it like an atom over here who puts everything on the credit card you know it’s easy to go over that three thousand dollars every month it is and I mean that’s when it’s important for your lender to make sure that they’re working with you and getting documentation to show that you paying that off every month or it’d be good idea to maybe make a payment before you have your credit pulled oh yeah or call the credit card and try to get your limit raised that’s another great idea I mean we do that in certain situations too where somebody’s carrying a balance and we’re over that 30 percent threshold you can always call your credit card and ask for that high credit to be raised and does that affect your score though because now you have it does not okay it does not so that’s something we’ll talk about later – the difference between a soft pull on your credit and a hard pull on your credit so basically amounts owed 30% if you get over 50% your credits gonna take another hit if you get over 75 edit card balance yes your score is gonna take another hit so those are the the threshold markers that they’re looking at so obviously the goal is to keep it below 30% so we’re at 65% of your total score right now just off of those two but they said just a mouth so it’s not just credit cards it’s your auto loans installment loans yeah so the algorithm that they use is this really fancy algorithm that nobody can get the key to it they develop this that you know Experian TransUnion Equifax or billion-dollar companies they’re not going to give the key out to their algorithm but from what we understand is as they look at it in the within the algorithm as individual accounts what is your usage ratio and then they take it as a whole and what is your usage ratio with all of your outstanding debt out there and that they both play into what your credit scores are going to be so I’m confused because under amounts owed one of your example you have is mortgage loans yes which to me insinuates that the more mortgages I take out the worst my credit score would be but as amounts owed and and when you’re talking about mortgage loans is it really more about like that income ratio not not debt to income ratio but because once again your income has nothing to do with this but it’s more about the ratio with your high credit limit so to answer your question if you have multiple mortgages on your credit report that is gonna affect your usage ratio but as long as you’re paying them on time it’s not necessarily gonna – your credits not gonna take a hit enough to affect you at all if it’s not my income then what are they comparing the amount the total amount of mortgages that I have outstanding what are they comparing yeah I’m not you oh so it’s because it’s the total amount that you owe today oh right yeah that’s getting bigger right when you take a mortgage out let’s say you get a $200,000 mortgage okay so as you pay on that the balance is going to slowly come down you know very slowly there 10 years of a mortgage most of your payment has gone towards interest whereas the last you know five to seven years of your mortgage the majority is gone towards paying your principal down but as long as I’m making my mortgage payment that’s what’s helping me with that that’s what’s helping you with your payment history but it it is is there a calculation as far as like the amount owed and how they calculate it so if I have $50,000 of available credit and I’m but or I don’t even know because mortgage loans auto loans I mean so it all yeah it all goes into that egg once again it’s that algorithm that none of us have the keys to that and Shannon you had talked about this earlier when we look at annualcreditreport.com and we look at a mortgage company and we look at a credit card company we are all pulling different algorithms so when you go to a lender and you’re applying for a home loan our algorithm is probably the toughest one so just because Discover card may say that you got a 780 credit score doesn’t mean that when I pull your credit as Endeavor Capital Mortgage you’re gonna have a 780 credit now why is that once again it all goes into to the algorithm we as a mortgage company are looking a little harder at your credit score and we’re putting more weight into certain categories because obviously you’re you are or then the model the model is automatically the mortgage model yeah it has a mortgage model it has an auto model it has a better general consumer yes credit card model and then it has just a and over and over all which is basically I think what our people are seeing yeah so ours is probably the toughest because your ability to repay is a huge thing for us in the mortgage business I mean that’s one of the biggest things that we’re looking at when we approve you for a loan so what has more weight on the mortgage model um probably I don’t know for sure but I’d probably say your payment history is probably the the thing that we look at the most you know because once again we’re trying to prove a track record of how have you paid in the past to accurately make a decision on you know should you get this loan or not and at what interest rate should you get this loan you know once again interest rates in today’s world a lot of people you’ll hear on the radio or TV or whatever they’re spouting off an interest rate and there’s no one interest rate that fits everybody everybody’s a little different there’s several different factors that go in to your interest rate when you’re getting a loan you know so I don’t ever quote just a random interest rate because I need to sit down and talk to you and look at your individual situation what is your credit score Adam you brought up debt to income ratio that’s an income ratio plays into that factor so there’s a lot of different things that’ll determine what kind of interest rates you get okay just just to be clear because I’m not sure that I fully understand if I have an auto loan should I pay it down more and that’ll raise my credit it would raise your credit if you want to pay it down more because it would help with your credit utilization ratio I don’t know from a financial perspective that that’s the smartest thing for you to do especially if you’ve got a really good interest rate but we’re kind of getting into a financial planner discussion there on what would be the best way to utilize your money okay so don’t just just be so frustrating like this is your whole life everything plays into it yet we can’t we don’t know no well I think he’s saying like everyone’s different so he doesn’t want to tell you know me for example to pay down my auto loan when he doesn’t know if I’ve got some big credit card debt out there that I haven’t been paying down and I’m carrying at it yeah it’s a hard puzzle yeah totally it’s definitely hard considering how much everything relies on this it’s a very difficult puzzle well that’s kind of I think that’s the idea of why we’re doing a second podcast about it and why we’re encouraging people to make you know take the time to really look into and think about it and kind of take their credit score seriously because it seems like you can do a few little things to really hurt it or you can really do a few little things to really help it you’re exactly and why not take the time to try to help it because you might not need it right now but you’re gonna need it at some point yeah and hopefully you always need it your auto insurance I’m yeah I mean like you might not be trying to buy a new car right now or a new house right now but you are probably eventually and like just like you’re saying every day it’s infecting you because now the insurance and all that stuff and we’re going we want to educate you know you listeners out there on what are the right questions to ask when you’re sitting down with somebody so you understand if you can get a grip on this model just a little bit you’re going to understand what questions you know you need to ask and that that’s all going to help you in the long run so let’s see moving in our third piece here we are on your length of credit history which accounts for 15% of your score so then we’d be at 80% overall your length of credit history simply is how long have you had credit we’ve we’ve talked a little bit here about people who pay in cash and don’t have any credit at all so naturally someone who’s younger is just gonna be at a complete disadvantage because they’re just starting out in life yeah so what we try to do is is we try to set them up immediately with maybe like a secured credit card so the difference between a secured credit card and a regular credit card is that regular credit card maybe gives you the $10,000 limit and you can go run that credit card up quick and I’m sure we all did that when we were in our younger days if you get a secured credit card that’s going to a bank and actually giving them $500 and they hold that $500 and then they will issue you a secured card where your high credit limit is only $500 and what that does is that gives somebody the ability to fill the car up with gas go get their groceries every week and pay that off every month and you’re establishing a track record on your credit record history payment let me ask you because naturally I mean someone who just turns 18 or someone who’s coming out of college probably doesn’t have a lot of credit history just because the nature of the game right so have you seen would you recommend that maybe a parent get a secured credit card for a teenager 100% so something that they can start creating a credit history at the age of 10 11 12 13 I would probably say more you know college years maybe or you know when you’re 18 to start doing that why not younger so I mean that history is like should I take out a serious I take out a credit secured credit card in my newborn and that’s a great question that we need to do a little research on because I don’t know if there’s an age limit on what they would allow you to do because obviously not a secured credit card yeah because we want to put that card in the person’s name and I think you have to co-sign but but then I couldn’t just like let it sit there I’d have to actually be buying stuff in the room you actually want to use it I mean we want to see you sign her name yet but I can sign for her right now yeah sign for Cosette is a KO you’re not doing account authorized user’ on their time so we can do a little digging on that and and get I’ll get back to you guys maybe we can post something I mean a lot to that this is me being like an overprotective helicopter parent or whatever but I’m like maybe I’ll take out a credit card and her name and then use it like just to buy her diapers or something and pay it off every month you know hey I have to have it I would have to have it set up to auto pay off like from my bank account so I don’t remember it I don’t want to hurt her credits exactly we don’t want to yeah when you were six months old your diapers this mom okay well so you’re gonna look into that a little bit yeah I’ll look into that and then we’ll we’ll update everybody and post something how cool would that be if she turns 18 and she’s got like an eight 50 credits yeah awesome right hopefully if she has financial like where wherewithal or whatever because I don’t want her to go hey I’ve got this great credit score I got this great credit card let me go buy shopping that’s part of educating kids on finances yeah she will be well educated she’ll have to listen to every podcast she’ll be hitting Daddy up for down payment money – at that point for that in first house okay so what’s the next one new credit so the next one is new credit so now we’re up to that’s ten percent of your score so that’ll put us up to 90 percent now so new credit is when you go out and you apply for a new credit card or you apply for a mortgage or a car loan or anything like that so this is this is interesting when you apply for a mortgage the credit bureaus algorithm factors in that you’re probably going to be shopping for that mortgage and you make all three different lenders so when your credit gets pulled a hard inquiry a hard inquiry that does drop your score by a couple points nothing major but you do drop a couple points when that happens forever no it’ll build back up it’s just an initial hit because you’re having your credit pulled but if you go to let’s say two other lenders and also look your score is not gonna be hit again the second time and then hit again the third time isn’t that like as long as it’s within a certain period of time as long as it’s in a certain period of time and they go back and forth with that the last I’ve checked it’s 45 days that you’ve got that 45-day window same holds true for when you’re buying a car you know they’re expecting you to shop and look around to try and find the best deal for yourself what we don’t want to happen is we don’t want you to go out and apply for four new credit cards within a thirty day period that’s gonna that’s gonna whack your score is that hard that would be yeah so when you’re when you’re applying for a new credit card they are going to look at your credit and it’s gonna be also credit cards aren’t lumped together like they do mortgages or autos when you’re assuming you’re shopping around but the credit card situations at ding every single time every single time that you’re that you’re trying to open a new card and it goes back shannond you had brought up a point if we’re raising the credit limit if you have a credit card already and you’re asking for your credit limit to be raised generally that’s a soft pull so they’re not making a hard pull they’re they’re doing what’s called a soft pull so will not reduce your credit score if you’re asking what’s truly the difference between the hard and the soft pool because the hard pull is gonna affect your score that’s gonna drop your yes information information a lot of times if you’ve got a creditor that you’ve already got to establish credit with and they’re just looking at your score or they’re looking to approve you for a higher amount or you may notice that you got a Capital one card you’ve already got that one Capital one card but all of a sudden now you’re pre-approved for the quicksilver Capital one card and what they’re doing is is they’re doing a soft pull and they’re looking at you saying they’re paying their bills perfectly on this one credit card so we’re gonna go ahead and extend them another credit card so it’s just the information that’s pulled is very specific to them and the history for that specific creditor they don’t see every creditor that’s what they see your score and then their history yes specific history so it’s very interesting how they can do that and it shows you too that you can get into a lot of debt if they start pre approving you for all these credit cards and you’re getting these credit cards in and you’re activating them once again that’s multiple new sources of credit that you’re activating and that will bring your score down a little bit it’s weird because it will bring it down temporarily but then you have these like if you’re paying them off then you’re sort of helping your payment history right and your you’re like credit limit and all this can either stay so once again it’s confusing I mean I’ve been doing this 25 years and have taught this miss behind your credit score class forever and there’s always new changes coming about they’re changing the algorithm all the time but it’s a proprietary formula that they’re they’re billion-dollar companies they’re not going to give up their secret sauce so all we can do is try and interpret it the best we can and educate consumers out there on the best way to try and keep moving your credit score out so wait and let’s go back the length of credit history a little bit because we got off track on trying to establish our kids here but at the same time because I know it’s something with all these different credit card offers and points and and situations change in life and now maybe I want to Marriott versus this you know Southwest card or something of the sort to start building Marriott points for vacations or whatever but it’s very important the length of define that because it’s not just that you’ve gotten credit since you’re 18 and I’ve been on the credit scale for the last 25 30 years it’s it’s how long have you had that one specific credit card that really plays into that because after a while some of that stuff just falls off yeah and you bring up a very interesting point that I’m glad we’re going back to it one of the other big myths out there is I’ve got this credit card I really don’t use it a lot anymore I’m just gonna go ahead and close it down so once again our traditional mindset is well that’s that’s smart cut the credit card off close it down that way I’m not going to use it what we don’t realize is that hurts us in in several ways in the credit scoring model when we close that credit card down that had a $10,000 high credit limit and that we’ve had for 15 years that we’ve had for 15 years so it’s helped us with our length of credit history and it’s also helping us with the credit utilization rate because when they’re looking at it from a cumulative basis that $10,000 when you close that all of a sudden your high credit just went down by $10,000 so whatever balances you may be carrying now that utilization ratio has gone up 30% of your score that could affect you so once again one of the the big myths out there is I’m just gonna close this credit card down and what we say is is don’t close it down leave it open we want that left open if you got to cut the credit card up so you don’t use it do whatever you’ve got to do but don’t close that card down but you do need to use it a little bit don’t you do yes you do need to use it if it goes dormant you know it’s not going to factor that much into your score it won’t ever just fall off unless you had physically closed the card down I think they do close it down like one of the things I was asking about is I had some store credit cards I think it was an old navy one and I haven’t you know okay so I had a credit card that we used to use for the company credit card and now I got a different credit card two years ago and I moved most of the stuff over but I just noticed the other day there’s like a four dollar charge that is recurring on that old credit card every month I mean I know what it’s for it’s good yeah but I’m like I guess I should keep that you should keep that yes I mean I like that card and I might as well keep that bill being charged to that card yeah instead of moving that bill to this to our new card I think that would probably be a smart thing to do out you know I would want to look at your overall profile before I gave a final judgment on that but I based off of what you’re saying I think that would be smart since you’ve had that credit card for a while you’ve got a length of credit history established and you probably have a high credit limit on there too that we don’t want to lose that okay okay and that like $4 monthly charge is better than having zero multicharts activity it’s it’s any kind of activity as long as you’re showing activity every month yeah let’s do your auto pay so you don’t forget about it $4 dollars so the last 10 percent of your score to get us to our full hundred percent here is the type of credit used so in the algorithm once again they are looking for their perfect blend of a mortgage a couple of credit cards an installment loan and when I say an installment loan that’s a car loan or anything that has a closed and well you’re financing something for your furniture for years at a certain interest rate you’re making a set monthly payment so they they are looking for that perfect little blend so if you’ve got just all credit cards and nothing else that’s not gonna play as well as if you’ve got a mortgage two or three credit cards and a car loan so that that’s what they mean when they say types of credit used you know they want to see that balance in there so and this is one of those things to just kind of it plays into that hard puzzled because now I’m trying to mix it all up and I’m putting more on my play I’m trying to get an installment loans I’m trying to get you know the mortgage loan they auto loan all these different perfect mix to create this pie yeah and you know what Shannon I don’t know if there is a perfect mix I mean that that’s where everybody gets people who really I want to busy enough but then late and now I’m have to play this game right I want an eight hundred credit score what do I have to do to get an eight hundred credit score you don’t need an eight hundred credit score would that be great yes but if you’ve got a 760 credit score you’re gonna get the premium interest rates out there for your mortgage for your car loan for your credit cards so a lot of times we get fixated on trying to get this perfect and we’re never gonna get it perfect so I think following this pie chart the best we can and being advised by somebody that understands credit we have some great software at Endeavor Capital where we can actually it’s a credit simulator so Adam if I ran your credit score and I wanted to try and get your credit score a little higher for whatever reason I can run you through this credit simulator and it’ll say pay down this credit card by this amount or transfer a balance from this credit card to this credit card and what it’s doing is it’ll increase your score by X number of points I want to do that because even though you say it sounds like anything over 760 doesn’t matter I want that I think eight thirty I want that have you ever really seen a fifteen wouldn’t that be an impossibility one twenty-five years the highest score I’ve ever seen is in eight fifteen I want that you want that we’ll get up we’ll get you there let’s do this credit simulator thing for we’ll get you there okay we’ll put your gear on it bet on the plate I’m gonna have to take out a student loan madam you need to take some college classes [Laughter] okay interesting so hopefully that was some good information for everybody out there on it at least you know helping you understand it a little better what are the right questions to ask and if you are thinking about buying a house or getting a car you at least know what you you know you should be doing and once again I can’t reiterate enough you go to the doctor once a year for your checkup all of our clients that Endeavor we do a mortgage checkup every six months so we take a look at what our current market rates and what is your interest rate and either we’re gonna recommend that you refinance because it looks like it’s in your best interest financially or you’re you’re looking great you know we can we can’t match the rate that you already have but don’t forget to do that with your homeowners insurance shop your homeowners insurance every year especially if you’re working on your credit score and you think your credit score has increased for whatever reason that year there’s a good chance you could get your premium lower okay love it so don’t forget to get your credit reports at annualcreditreport.com and then the other website that we talked about in the class was that I I’ve done this opt-out pre-screen what’s that so you can opt out of all the credit card offers all right now it does not keep your current credit card companies from selling your information or sending you offers which is what annoys me but yeah but you know yeah it just cuts down on a lot of the junk I want to cut down on the junk phone are the capital ones that keeps you know something something every day yeah yeah that definitely helps that’s a great site to go to and put your information in there George Damir what’s your phone number three one four three seven eight zero three three one what would you want people to email you they can email me at GDemare@ecapmortgage.com wonderful the myths of credit score everybody thank you for listening thank you thank you guys for having me and give us a call for any of your real estate or mortgage needs and take care

CLICK HERE FOR PODCAST

CLICK HERE FOR PODCAST